Recently, Public Bank wrest its muscle to attracts depositors to place their money with them. This has becomes an annual promotional event to get as much deposits after Chinese New Year. The reason was simple: CNY Ang Pow money... What is so exciting this round?

Yes. Depositors can get up to 8.88% p.a. interest on a step-up basis on the 12th month. Can you get it? It's 8.88% p.a. on the 12th month ONLY, not the whole tenure.

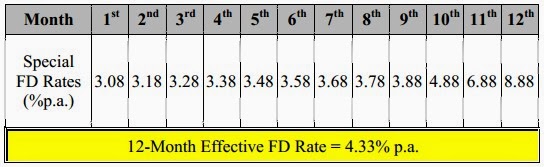

So, what's the EFFECTIVE rate that I can get?

Please refer to the below picture...

Not bad what... Wait... This is only on the 80% FD portion. If you add in the 20% SA portion to the whole principal that you have placed, it's lower than 4.33% p.a. actually. Anyway, it's still better than most FD rate offered by other banks. Cheers to Public Bank !!!

How about the FD rate after 12 months?

It will be auto-renewed according to the normal 1-month FD rate by that time (3.08% p.a. currently). So, if you don't like the 1-month FD rate offered, remember to uplift your money after 12 months ya ;)

What if I withdraw within 12 months?

You can do so. But, the interest paid (which is more than the prevailing FD interest rate) will be claw back. Please refer to below example.